Back

Published on April 04, 2022

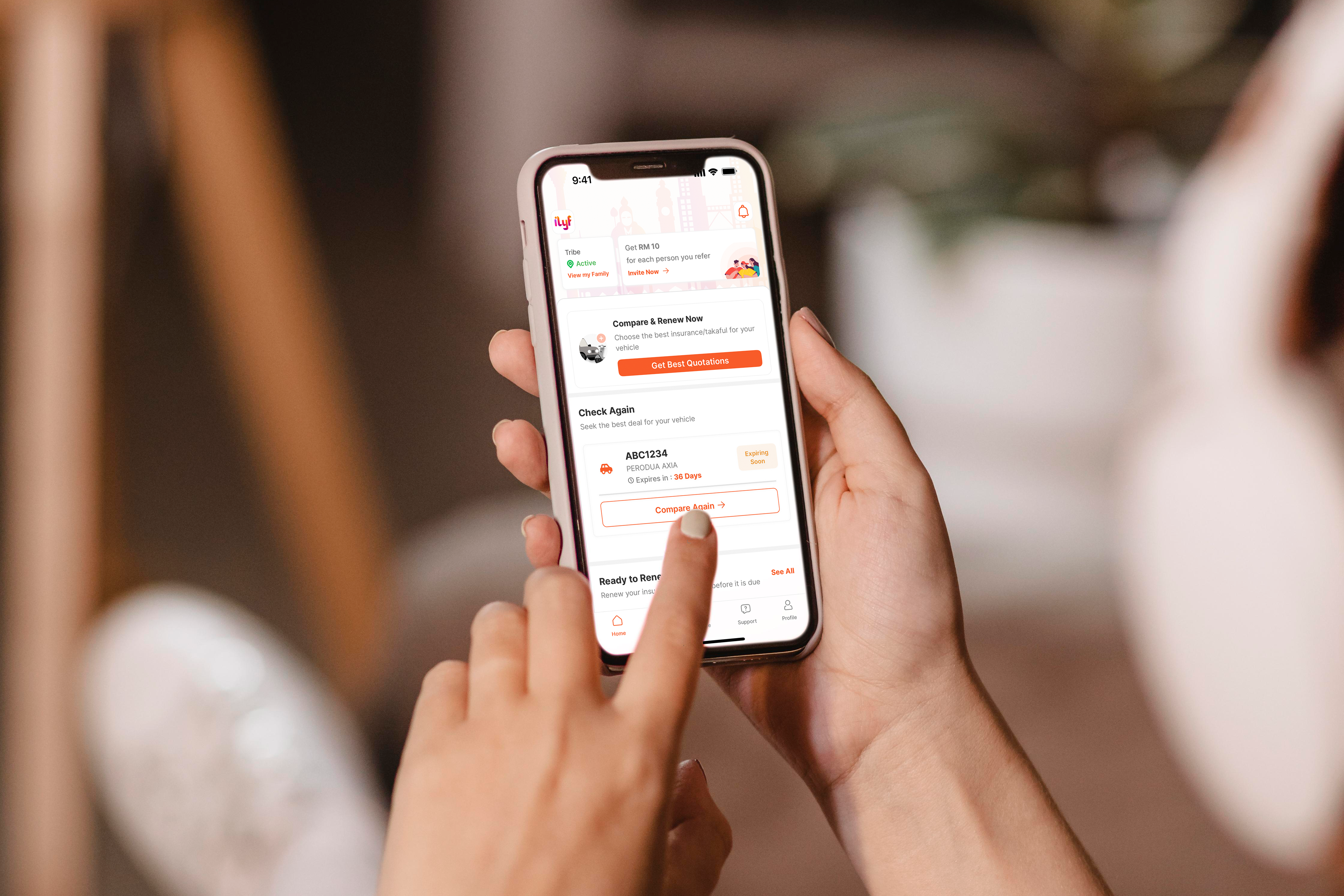

14 Quick Facts on Car Insurance!

- Car insurance is a policy contract signed between you and the insurance company that protects you against financial loss or damage in the event of a road accident or theft in exchange for annual premium payments.

- Before you decide what type of car insurance you want to purchase, you need to know the different types of policies available in the market. Bear in mind that any car insurance will not cover certain losses, such as your own death or bodily injuries due to an accident.

- Your liability against claims from passengers in your car and loss or damages arising from natural disasters are not covered as well.

- Another important factor that you should note is to be very honest to your insurance provider.

- Should you fail to disclose any details, your insurance company has the right to refuse to pay your claim or any claims made by a third party against you.

- When in doubt, always check the insurance policy for full details on exclusions.

- The insurance policy is effective from the time of purchase or at the agreed time of commencement, until the expiry date.

- A standard SST rate of 6% is chargeable on top of the insurance premium, to be applied before stamp duty.

- A stamp duty fee of RM10 is levied on top of the car insurance purchase before the final payable amount is generated.

- A stamp duty fee of 10% of the premium is chargeable if the insurance policy was purchased through an agent.

- The policyholder is required to pay SST and Stamp Duty before the total insurance premium price is calculated. For example:

- Insurance Premium Gross Total (After discounted with NCD): RM2,000

- SST (6%): RM120

- Stamp Duty: RM10

- Total Annual Premium: RM2,330

- It was decided that the liberalisation of the motor and fire tariffs would be implemented in a phased approach to make time for consumers and industries alike to adjust to the new operating environment.

- The rule of thumb is to ensure the vehicle at its current market value.

- The insurer will only bear part of the loss in proportion to the difference between the market value and the sum insured based on the formula below:

Loss Amount Payable = (Sum Insured / Market Value) × Assessed Loss

For example: Let’s say the policyholder had set the sum insured of the vehicle at RM50,000 instead of the market value of RM60,000. Keep in mind that this will only apply if the under-insured amount is more than 10% of the market value.

Share :

Latest Post

SyncWealth Sdn Bhd202101028803(1429103-H)

Unit 3.07, Level 3, KL Gateway Mall, No 2, Jalan Kerinchi, Pantai Dalam, 59200 Kuala Lumpur, Wilayah Persekutuan Kuala Lumpur.

81 Ayer Rajah Crescent, #02-59 JTC Launchpad, Singapore 139967.

Features

Gadget Insurance

Travel Insurance

Home Insurance

Pet Insurance

Auto Services

Resources

Download App

Follow and Contact Us

© 2026 SyncWealth Sdn Bhd All rights reserved. v3.12.2